Yes, you absolutely can. And it can happen even when you're getting bookings, even when the property looks great, and even when your spreadsheet shows a high gross yield.

The good news? Losses on Airbnb investing are usually predictable. They come from a small set of repeatable mistakes in underwriting, compliance, and operations. This guide will help you avoid them.

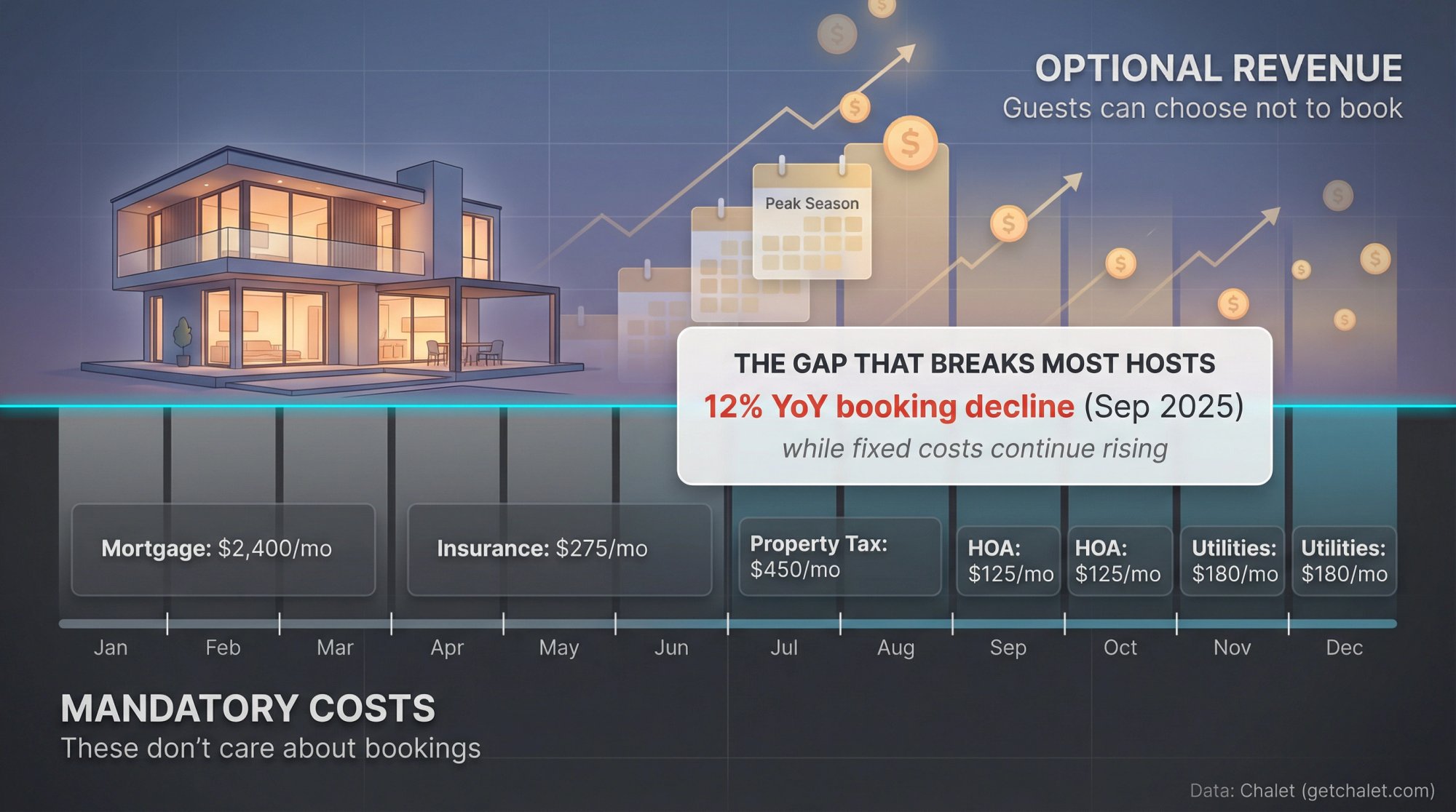

There was a time when buying a property and listing it on Airbnb felt like a guaranteed wealth builder, fueled by low interest rates and social media success stories. But that wave is breaking. Recent market data shows occupancy rates falling in many markets (bookings in September 2025 were about 12% lower year-over-year), while costs keep rising. The math that worked in 2021 doesn't work anymore for most STR markets.

This changes your approach to STR investing from "will this make me rich?" to "how do I not lose money?"

That's what we'll cover.

We'll treat an Airbnb rental (often called a short-term rental or STR) like what it really is: a small business sitting on top of real estate. That framing matters because it shifts how you think about risk, operations, and profit.

How Do Airbnb Investors Lose Money?

People use "lose money" three different ways. You need to know which one you mean.

1. You lose money on monthly cash flow

This is the most common fear. Your cash coming in is lower than your cash going out, so you have to cover the gap from your paycheck or savings each month. It's not sustainable for long.

2. You lose money on exit

Even if you survive month-to-month, you can lose money when you sell:

• You sell for less than you paid

• You sell for more, but transaction costs and taxes eat the gain

• You're forced to sell during a bad window (regulation change, insurance shock, personal liquidity event)

3. You show a "paper loss" on taxes but are cash-flow positive

This is the confusing one. Depreciation and cost segregation can create tax losses while your bank account is fine. (This is not tax advice. Talk to a CPA.)

This guide focuses mainly on real cash losses (types 1 and 2).

How Do Airbnb Rentals Make Money?

At the atomic level, this is the whole game:

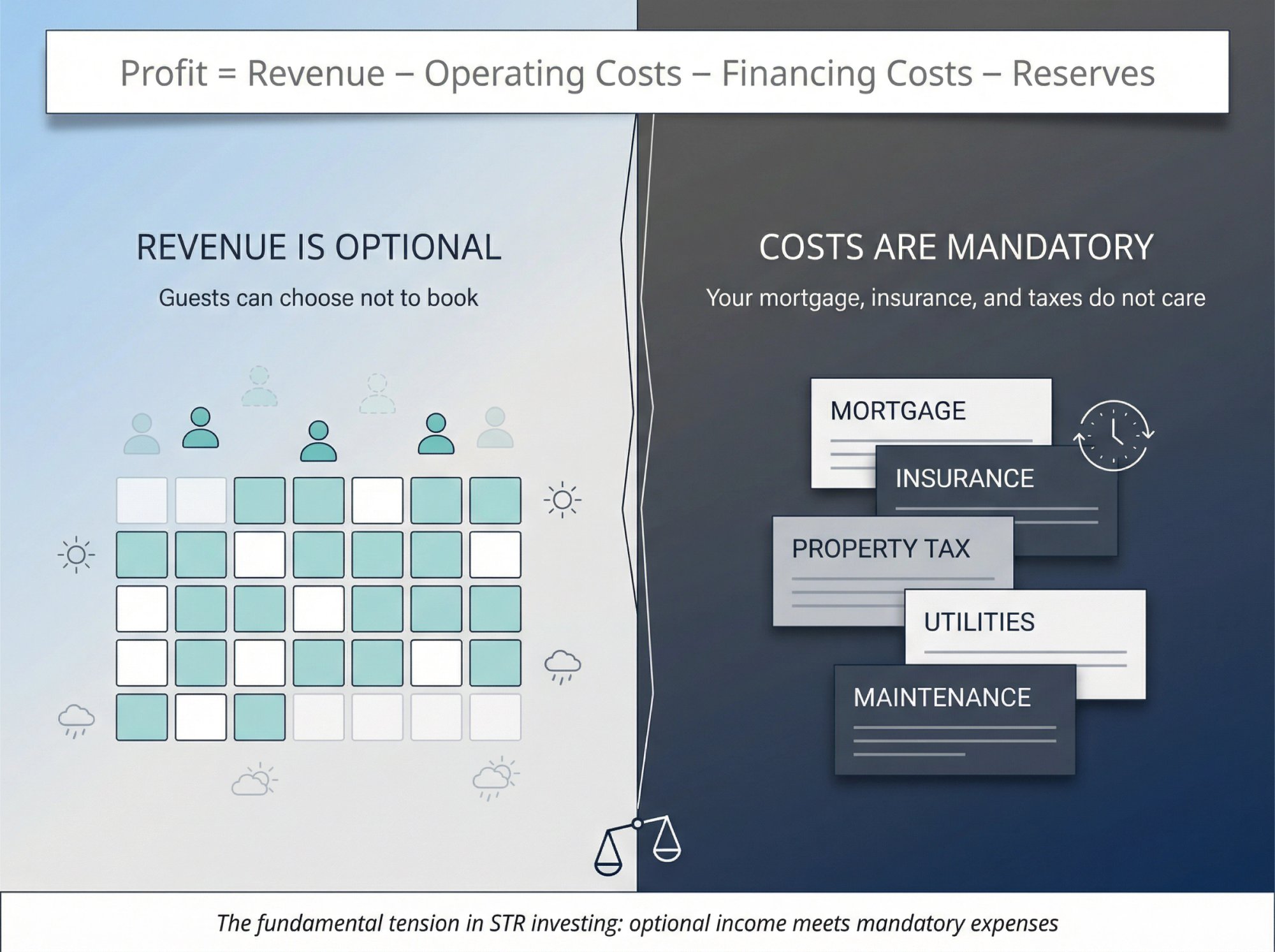

Profit = Revenue − Operating Costs − Financing Costs − Reserves

If your analysis is missing even one of those buckets, your "deal" is an illusion.

The Single Biggest Mental Model Upgrade

Revenue is optional. Costs are mandatory.

Guests can choose not to book. Your mortgage, insurance, and taxes do not care.

This is why STRs can feel amazing in peak season and terrifying in shoulder season. The disconnect between optional revenue and mandatory costs is what breaks most hosts.

Airbnb Profit and Loss Statement Template

Use this as your default profit and loss statement for underwriting any STR deal:

| Category | Line Item | Fixed or Variable? | Notes You Should Not Skip |

|---|---|---|---|

| Revenue | Nightly revenue | Variable | Base it on comparable listings, not "market averages" |

| Revenue | Cleaning fee revenue | Variable | Often pass-through; still impacts platform fees and demand |

| Revenue | Pet / extra guest / upsell revenue | Variable | Count only if truly common in your niche |

| Platform costs | Platform service fee | Variable | Fee structure can change; model it explicitly (Airbnb fee details) |

| Ops costs | Cleaning labor | Variable | Cost per turn + deep cleans + laundry |

| Ops costs | Consumables | Variable | Coffee, paper goods, toiletries, trash bags |

| Ops costs | Repairs and maintenance | Mixed | Small fixes + handyman + emergency calls |

| Ops costs | Utilities + internet | Mostly fixed | Often higher than long-term rentals |

| Ops costs | Pest control / yard / snow | Mixed | Seasonal, but real |

| Ops costs | Property management | Variable | Commonly 15-25% of revenue (research average) |

| Asset costs | Insurance | Fixed | STR policies differ from homeowners coverage (insurance cost analysis) |

| Asset costs | Property taxes | Fixed | Verify local rate and reassessment risk |

| Asset costs | HOA / COA dues | Fixed | Plus: STR rule risk |

| Asset costs | Licenses / permits / inspections | Fixed | Costs plus "can you legally operate?" |

| Financing | Mortgage principal + interest | Fixed | Affects survival more than anything (current mortgage rates) |

| Financing | Lender reserves requirement | Fixed | DSCR lenders may require reserves (varies) |

| Reserves | CapEx reserve | Fixed-ish | Furniture, HVAC, roof, hot tub, repainting |

| Reserves | Vacancy / seasonality reserve | Fixed-ish | Your "sleep at night" fund |

If you want to run these numbers quickly on a specific address, use Chalet's free calculator built exactly for this.

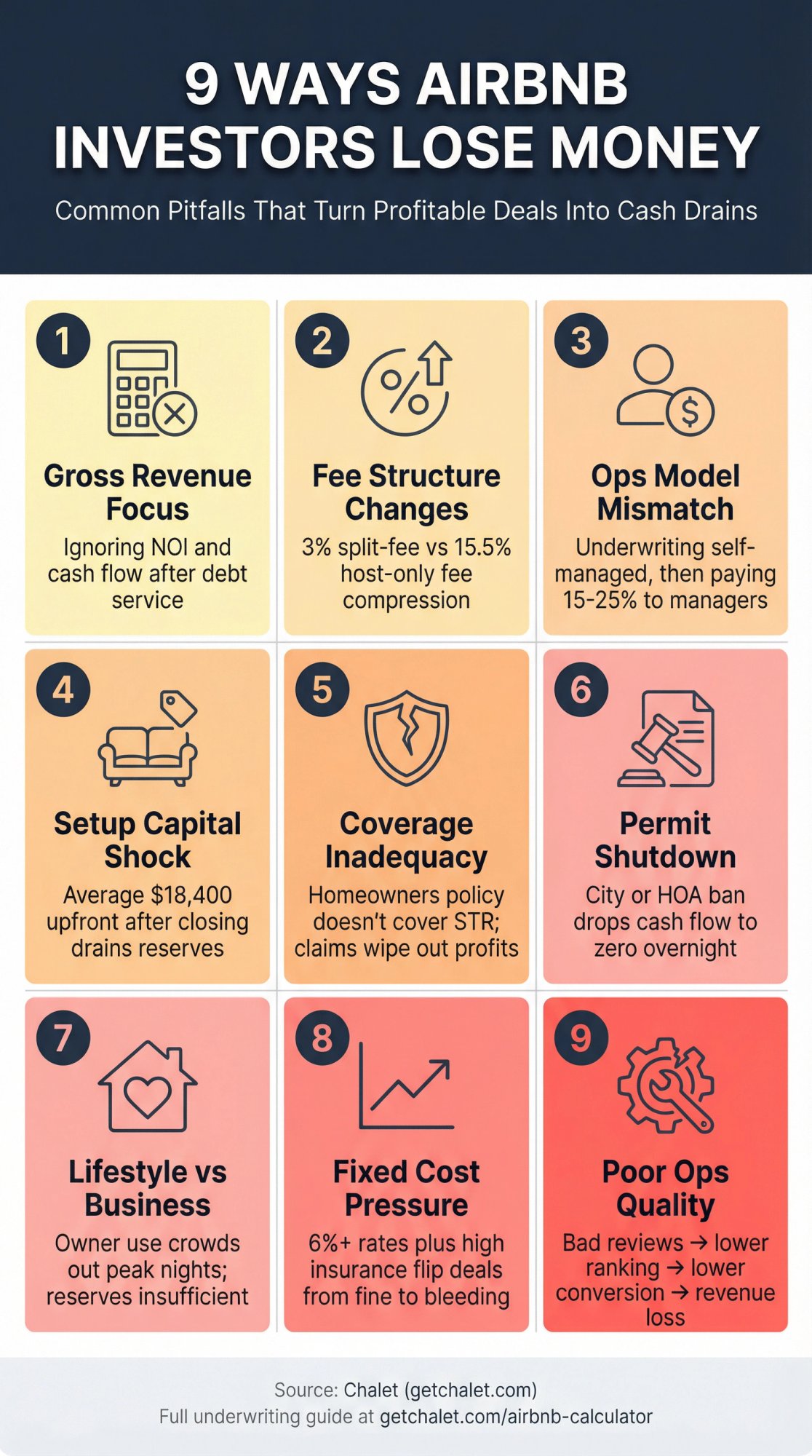

9 Ways Airbnb Investors Lose Money

1. Underwriting Gross Revenue Instead of Net Cash Flow

A lot of listings for sale look great on the top line. But if your underwriting is basically "annual revenue looks high, so I'm good," you're not underwriting. You're daydreaming.

Fix: Underwrite to net operating income (NOI) and cash flow after debt service.

• NOI = revenue − operating expenses (before mortgage)

• Cash flow = NOI − mortgage − reserves

Use Chalet's free Excel underwriting sheet if you like modeling in detail.

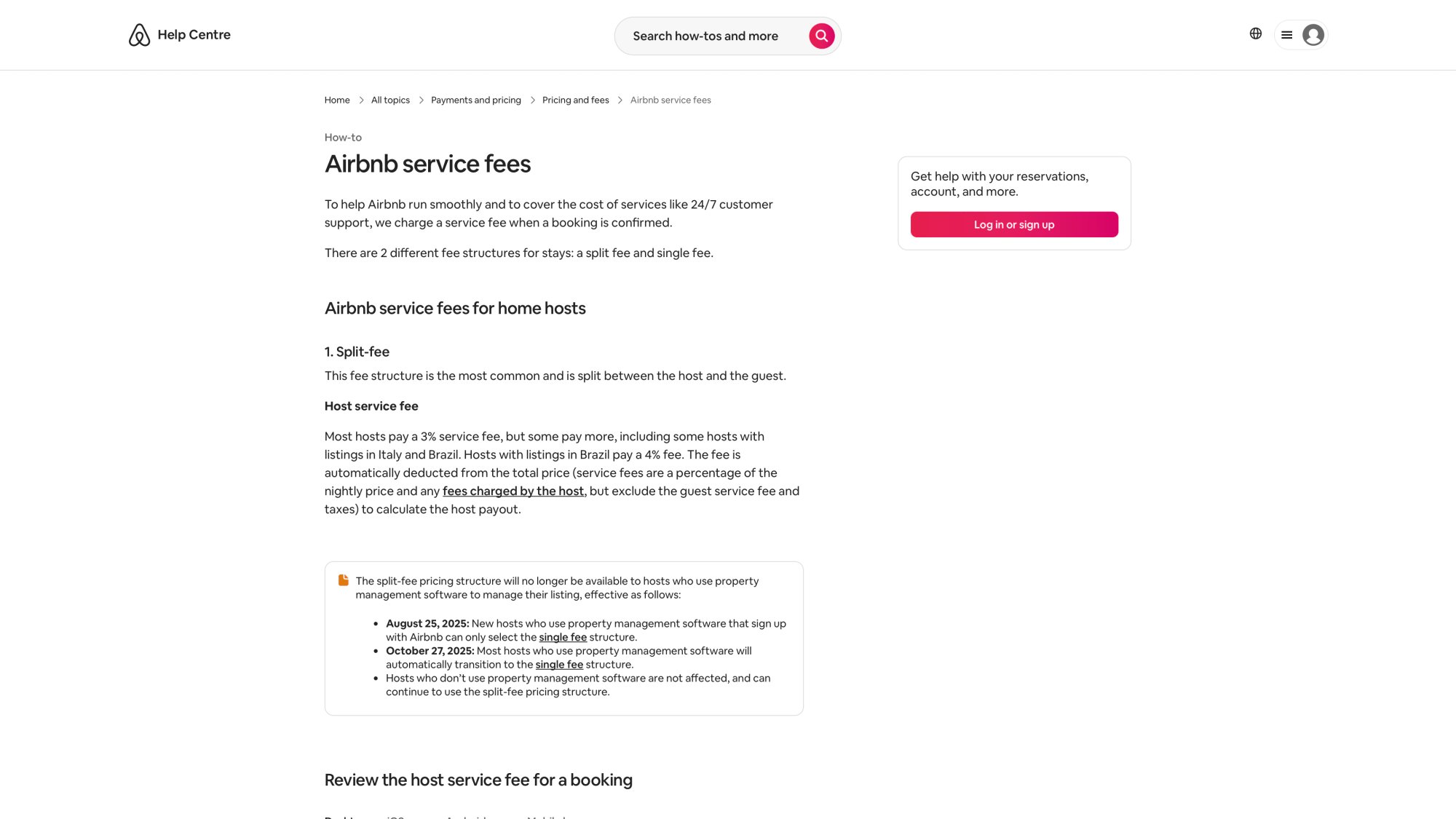

2. Platform Fee Changes That Kill Your Margins

Airbnb has multiple fee structures, and the details matter.

Most hosts pay about 3% under a split-fee structure (where guests pay a separate service fee), but there's also a single-fee structure where the fee is deducted from the host payout at 15.5%.

Why this causes losses: if your pro forma assumes a small host fee and you end up paying a much larger host-only fee, your margins compress immediately.

Fix: Model platform fees as a line item, and run "fee shock" as a stress test. A 10% change in fees hits you harder than a 10% change in gross revenue because fees come out before you pay fixed costs.

3. Self-Managing vs Hiring Property Management

If you self-manage, you pay with time and stress. If you hire management, you pay with margin.

Research shows that most Airbnb management companies charge between 15% and 25% of rental income.

The losing-money move: underwriting the deal as self-managed, then switching to a manager after three months when you're burned out.

Fix: Decide your operating model upfront.

• If you plan to hire a manager, underwrite with a manager

• If you plan to self-manage, budget your own "management wage" anyway, so you know what you're really earning

Need vetted STR property managers? Start here: Chalet's property management directory.

4. Furnishing Costs Most First-Timers Underestimate

Many first-timers treat furnishing like a cosmetic detail.

In reality, furnishing is often the biggest "surprise check" you write after closing. Industry research found an average total furnishing cost per property of about $18,400 (median $15,900), with wide variation by property size and market.

Why this causes losses: you buy a property that barely cash flows, then you drop $15k to $30k on setup and spend the next year digging out.

Fix: Treat setup as part of your all-in basis, and plan your launch timeline.

• Furnishing budget

• Starter supplies

• Smart locks and security

• Initial deep clean

• Photos

• First maintenance sweep (fix everything you can before guests arrive)

To line up furnishing and ops vendors, use Chalet's STR directory.

5. Why Homeowners Insurance Doesn't Cover STR Risks

This one is brutal because it's expensive when it fails.

Standard homeowners insurance typically does not cover the risks of renting to short-term guests, and short-term rental insurance is designed to fill those gaps. The National Association of Short-Term Rental Management cites an average premium between $2,000 and $3,000 per year.

Why this causes losses: a single claim can wipe out a year of profit, and an insurance cancellation can force you to stop operating or scramble for expensive coverage.

Fix: Get real insurance quotes before you close, not after. Need STR insurance options and guidance? Connect through Chalet's vendor network.

6. STR Regulation Risk Can Shut You Down Overnight

This is the "your business license is the product" problem.

If a city (or HOA) decides your STR is illegal, your cash flow can drop to zero overnight.

A Reuters report highlights how fast regulations can tighten. In Spain, the government ordered Airbnb to withdraw more than 65,000 listings it said violated rules, and Barcelona's mayor planned to ban all permits for short-term rentals by 2028.

That's Spain, but the lesson is universal: politics follows incentives, and housing pressure creates incentives.

Fix: Underwrite regulation like a core variable, not a footnote. Before you buy, verify:

• Is STR allowed in this zoning?

• Is a permit required?

• Is there a cap, lottery, waitlist, or renewal risk?

• Are there primary-residence rules?

• Does the HOA ban rentals under 30 days?

Use Chalet's regulation resources to check your target market.

7. Buying a "Vacation Home" vs Buying a Business

This is the most common emotional trap:

"I love this property. I'll use it sometimes. And it'll pay for itself."

That is a lifestyle purchase with an income side hustle. It can be fine. But if you underwrite it like a profit investment, you get hurt.

Fix: Decide what you are buying:

• A business-first rental

• A lifestyle-first second home

• A hybrid

Then underwrite it honestly. Hybrids need larger reserves because owner use crowds out peak nights.

8. How Interest Rates and DSCR Affect Airbnb Profits

Fixed costs kill STRs. Debt is the biggest fixed cost.

Freddie Mac's Primary Mortgage Market Survey shows the U.S. weekly average 30-year fixed-rate mortgage was 6.06% as of January 15, 2026 (and 7.04% a year earlier).

Even small rate differences can flip a deal from "fine" to "bleeding," especially when you also have higher utilities, higher insurance, and management.

Fix: Do three underwriting runs:

1. Base case: Realistic comp-based revenue and costs

2. Conservative case: Lower revenue, higher costs

3. Survival case: "If this is mediocre for 12 months, do I still live?"

If you want DSCR-friendly lenders who understand STR income, start here: Chalet's Airbnb loan network.

9. Poor Operations Lead to Lower Revenue

On Airbnb, operations are not a cost center. They are your product quality.

Bad ops cause:

• Worse reviews

• Lower ranking

• Lower conversion

• More refunds and support issues

• More damage

Which then causes lower revenue. And then you lose money.

Fix: Build a real operating system:

• Cleaning checklist + inspection photos

• Linen process (owner closet, off-site laundry, or service)

• Preventive maintenance calendar

• Pricing strategy (weekday vs. weekend, event spikes)

• Guest messaging templates and house rules

• Local handyman and emergency coverage

Chalet's ops and vendor directory is built for exactly this stage.

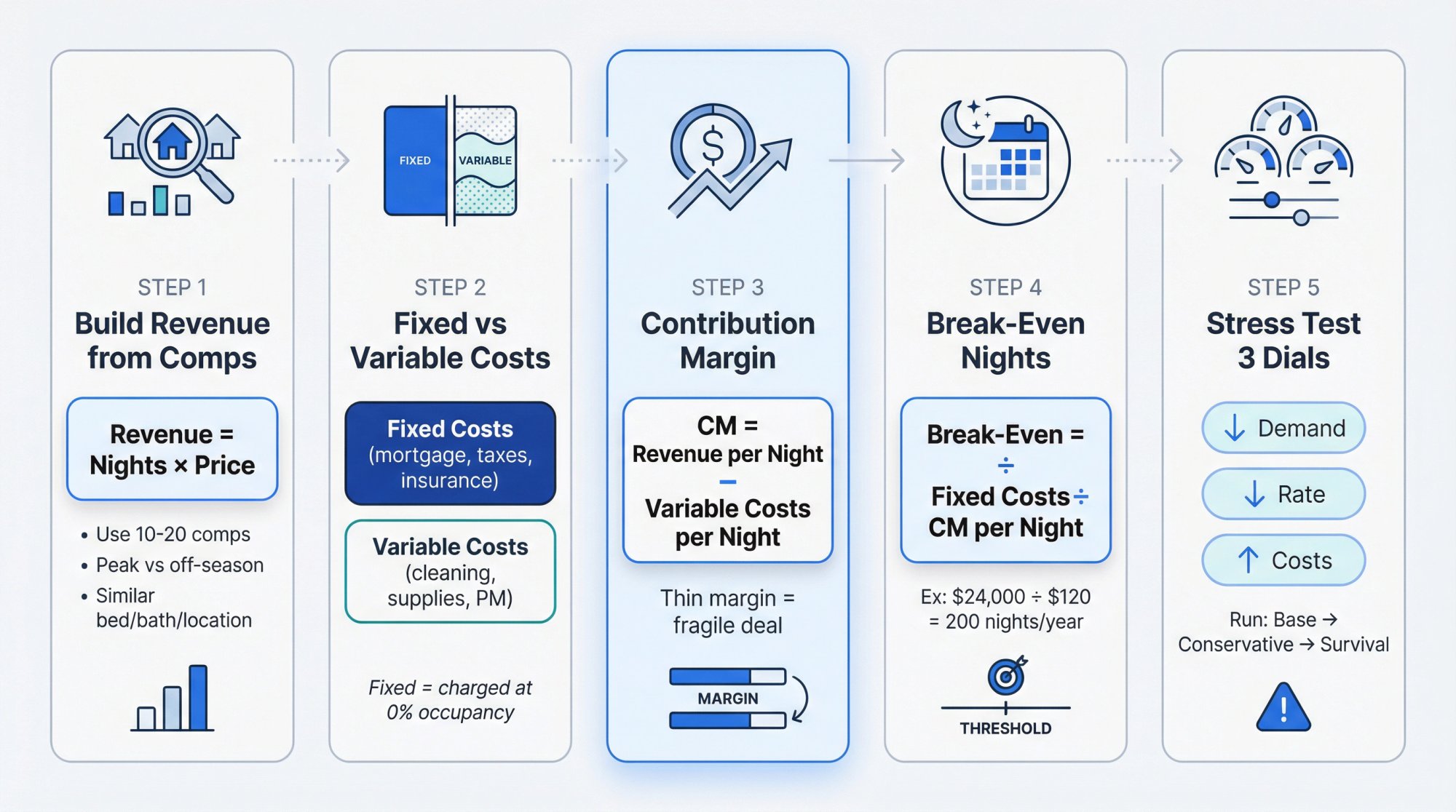

How to Underwrite an Airbnb Rental Correctly

This is the core "do it like a pro" workflow. It works for first-time buyers and portfolio builders.

Step 1: Build Revenue from Comps, Not Hope

Revenue = nights booked × price per night.

But "price per night" is not your listing rate. It's what you actually collect after discounts, seasonality, and competition.

Comp rules that prevent losses:

• Compare to similar size, bed/bath count, location, and amenity tier

• Look at at least 10 to 20 comps if possible

• Separate peak-season performance from off-season performance

• Treat "new listing boost" as temporary

Run this quickly by address: Chalet's free calculator.

Step 2: Separate Fixed Costs from Variable Costs

This is huge because it tells you how fragile your deal is.

• Fixed costs keep charging even at zero occupancy

• Variable costs mostly scale with bookings

If a deal has high fixed costs (high debt, high taxes, high insurance), it is more likely to lose money during slow periods.

Step 3: Use Contribution Margin (This Is the Cleanest Mental Model)

Contribution margin is:

(Revenue per booked night) − (variable costs per booked night)

Your fixed costs are paid out of contribution margin.

If your contribution margin is thin, your deal is fragile.

Step 4: Compute Break-Even Nights

Break-even nights per year is:

Break-even nights = Fixed costs / Contribution margin per night

This is the fastest way to sanity-check a deal.

If your break-even nights feels unrealistic for the market's seasonality, the deal is not safe.

Step 5: Stress Test the Exact Things That Break STRs

Use three dials:

• Demand dial (booked nights)

• Rate dial (ADR)

• Cost dial (management, insurance, cleaning, repairs)

Run a "survival case" where all three move against you at once.

| Scenario | Bookings | Nightly Rate | Operating Costs | What You're Testing |

|---|---|---|---|---|

| Base | Normal | Normal | Normal | Can it work as expected? |

| Conservative | Lower | Slightly lower | Slightly higher | Can it handle mild headwinds? |

| Survival | Much lower | Lower | Higher | Can you survive a bad year? |

If you want to model this with more precision, use Chalet's Excel tool.

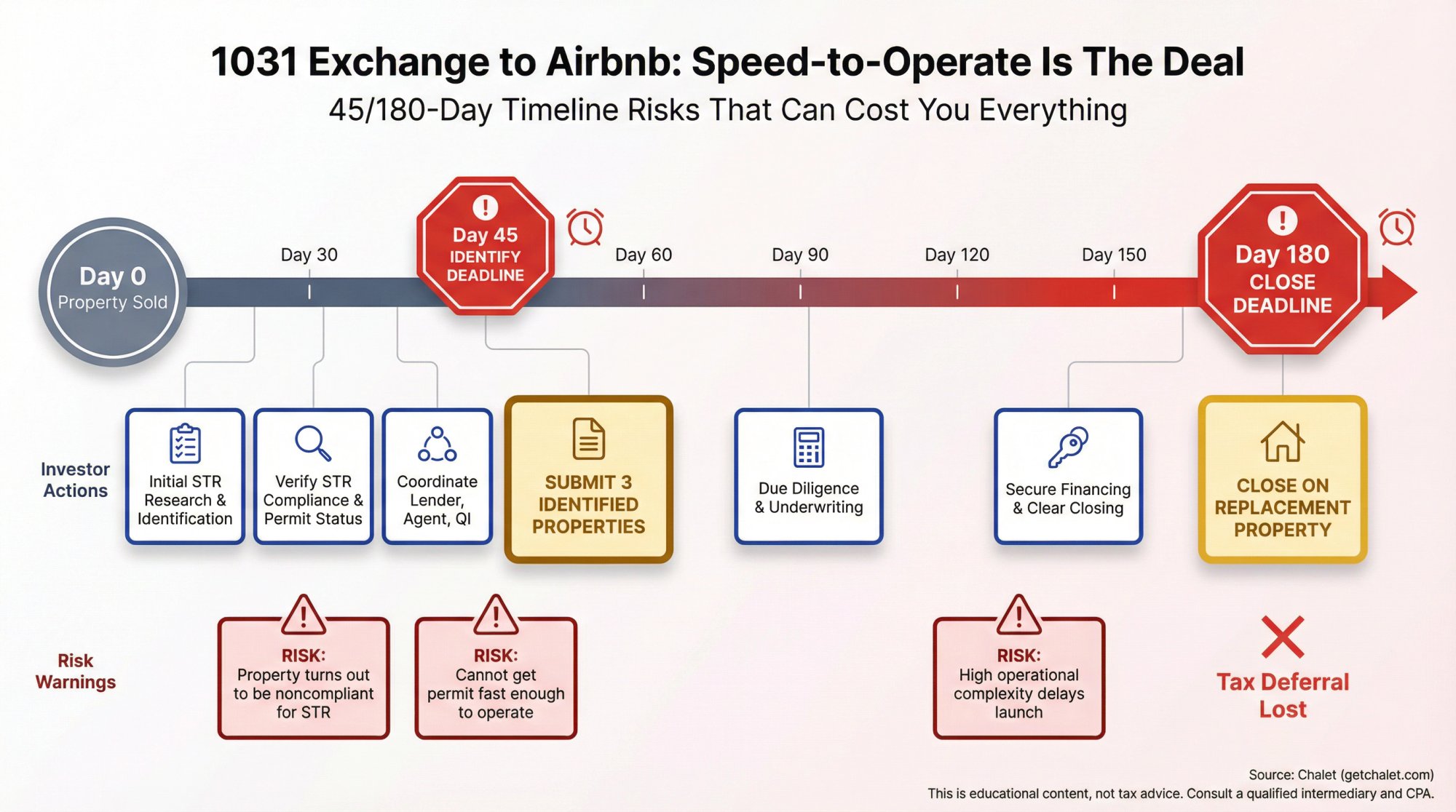

1031 Exchange Investors: Special Airbnb Loss Risks

If you're doing a 1031 exchange, your risk profile changes.

You can lose money (or lose the entire tax deferral benefit) by:

• Identifying properties that later turn out to be noncompliant STRs

• Buying something that cannot get permitted quickly enough to operate

• Choosing an asset with high operational complexity that delays launch

If you're on a tight 45/180-day clock, speed-to-operate is not a nice-to-have. It's the deal.

Use Chalet's exchange-oriented content and vendor network as your execution layer:

• Exchange-savvy agents

What to Do If You're Already Losing Money on Airbnb

You don't need motivation. You need triage.

1. Confirm whether you have a revenue problem or a cost problem

Pull 90 days of actuals.

• If occupancy is low, you have a demand or positioning problem

• If occupancy is fine but you're bleeding, you have a margin problem

2. Fix the "leaks" before you chase growth

Common leaks:

• Management fees + add-on fees

• Cleaning inefficiency

• Utility waste

• Over-discounting

• Deferred maintenance causing bad reviews

3. Consider a strategic pivot: mid-term rentals

If regulation or seasonality is killing you, mid-term rentals (30+ days) can sometimes stabilize cash flow (travel nurses, insurance displacement, corporate stays).

Chalet has a mid-term rental calculator if you want to run the pivot numbers. (And market dashboards too.)

4. If the asset is fundamentally wrong, plan an exit like a pro

Sometimes the right move is to sell. Not because you "failed," but because capital has opportunity cost.

If you're thinking about selling, start here: Chalet's STR sale resources.

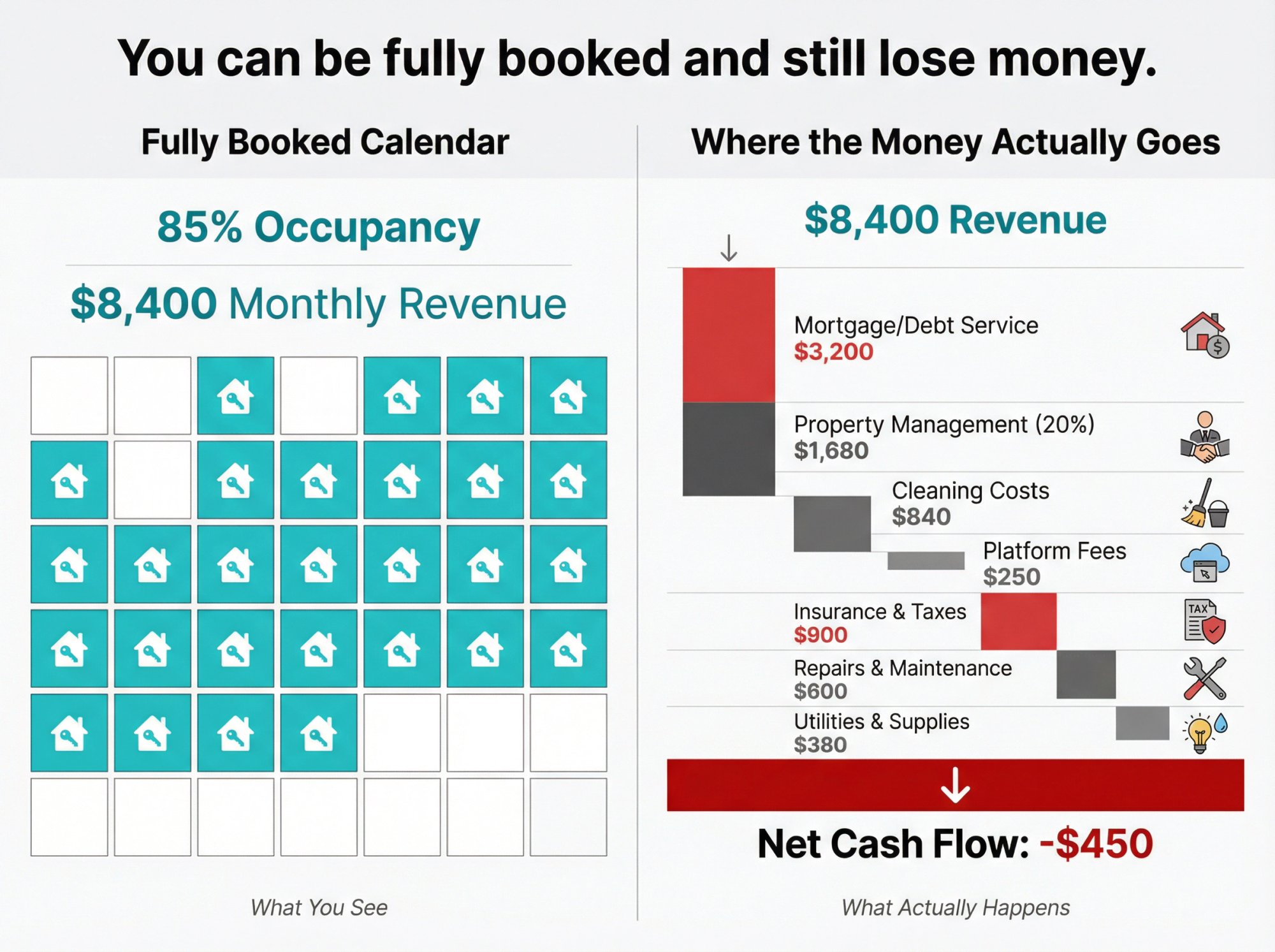

Can You Lose Money on Airbnb Even with Bookings?

Yes. Bookings do not equal profit.

You can be busy and still lose money if:

• Your fixed costs are too high

• Your management + cleaning costs eat the margin

• Your platform fee structure changed

• You're constantly repairing and replacing things

Does Airbnb's Platform Protection Replace Insurance?

Treat platform protection as a backstop, not your primary risk plan. Research notes that platform host protection is often limited in scope and hosts should review what is and is not covered and supplement with their own insurance.

Are Airbnb Investments Too Risky in 2026?

They're not automatically risky. They're more sensitive than long-term rentals.

STR cash flow depends on:

• Demand

• Competition

• Operations quality

• Regulation

That sensitivity creates both upside and downside. Your job is to buy the downside protection first: compliance, reserves, margin, and adaptability.

Next Steps to Avoid Losing Money on Your Airbnb

If you do only three things after reading this, do these:

1. Run a real underwriting (not just gross revenue): Chalet's calculator

2. Check local STR rules before you fall in love: Chalet's regulation resources

3. Talk to an STR-specialist agent who knows the gotchas: Chalet's agent network

If you want the "all-in-one" path (research → ROI → pros to execute), that's what Chalet is built for: free analytics plus a vetted vendor network so you can actually close and operate without guesswork.