If you're searching "Airbnb not covering mortgage," you're facing one of two situations. Either you already own a property and the monthly numbers keep coming up short, or you're about to buy and want to avoid a painful surprise. This guide addresses both.

The core mechanics apply whether you call it an Airbnb rental, a short-term rental, or an STR. The problem is universal: your mortgage is fixed, but your revenue isn't.

Why Your Airbnb Rental Income Doesn't Cover the Mortgage Payment

Airbnb doesn't cover your mortgage. You do.

The platform helps you find guests, process payments, and handle disputes. But it can't guarantee your income. And that mismatch is exactly what creates the problem most hosts face.

From first principles, here's what you're dealing with:

-

Your mortgage payment happens every month, whether you have bookings or not.

-

Your nightly revenue follows a probability distribution with highs, lows, and bad months. Plus tail risks (regulation changes, bad review streaks, competing supply waves, platform fee adjustments).

The only sustainable strategy? Build enough margin and flexibility so bad months don't break you.

How to Diagnose Why Your Airbnb Isn't Covering Your Mortgage (30-Minute Analysis)

Before you change pricing, buy new furniture, or refinance, you need to locate the leak. Pull these six numbers from the last 30-90 days (plus trailing 12 months if you have it):

1. All-in monthly housing cost

Principal + interest + property taxes + insurance + HOA (if applicable)

2. Average nightly rate (ADR)

What you actually achieved, not what you hoped for

3. Occupancy percentage

Booked nights divided by total nights available

4. Platform fees paid

The actual fees Airbnb charged you

5. Operating costs

Utilities, cleaning, supplies, maintenance, management, lawn/snow, pest control, trash, internet, subscriptions

6. Net Operating Income (NOI)

Total revenue minus operating costs (before mortgage)

Now calculate your Debt Service Coverage Ratio (DSCR):

DSCR = NOI / Monthly Mortgage Payment

This is what those numbers tell you:

| DSCR Range | What It Tells You |

|---|---|

| < 1.0 | Operations didn't produce enough to cover the mortgage |

| 1.0 to 1.2 | You're covering it, but living on a thin edge |

| 1.2+ | You have a cushion for volatility |

Most lenders want DSCR above 1.1 to 1.25 because it leaves room for the inevitable ups and downs. (Research from Rocket Mortgage explains the DSCR framework in detail.)

If you want a fast way to run this math on any address, Chalet's free Airbnb calculator is built for exactly this scenario.

The Mistake That Kills Most Airbnb Mortgage Coverage Calculations

When people say "my Airbnb isn't covering the mortgage," they're usually making one critical error:

They compare gross booking revenue to the mortgage payment.

That's wrong. The correct comparison is NOI versus mortgage payment (your DSCR).

Why? Because the mortgage gets paid after you operate the property. Cleaning, utilities, insurance, repairs, and platform fees come out first.

Use this cost map in your spreadsheet:

| Category | Examples | Fixed or Variable? | Usually Missed? |

|---|---|---|---|

| Debt service | Principal + interest | Fixed | No |

| Taxes + insurance | Property tax, hazard insurance | Fixed-ish | Sometimes |

| HOA | Condo/POA dues | Fixed-ish | Often |

| Utilities | Electric, gas, water, trash | Fixed-ish | Often |

| Internet + streaming | WiFi, YouTube TV, Netflix | Fixed | Often |

| Cleaning | Turnover cleans, linens | Variable | Sometimes |

| Supplies | Paper goods, coffee, soap | Variable | Often |

| Maintenance reserve | HVAC, plumbing, paint, replacements | Variable | Almost always |

| Management | PM percentage, co-host, admin | Variable | Often |

| Platform fees | Airbnb service fee | Variable | Often |

If you don't have a maintenance reserve line item, you're not doing profit math. You're doing hope math.

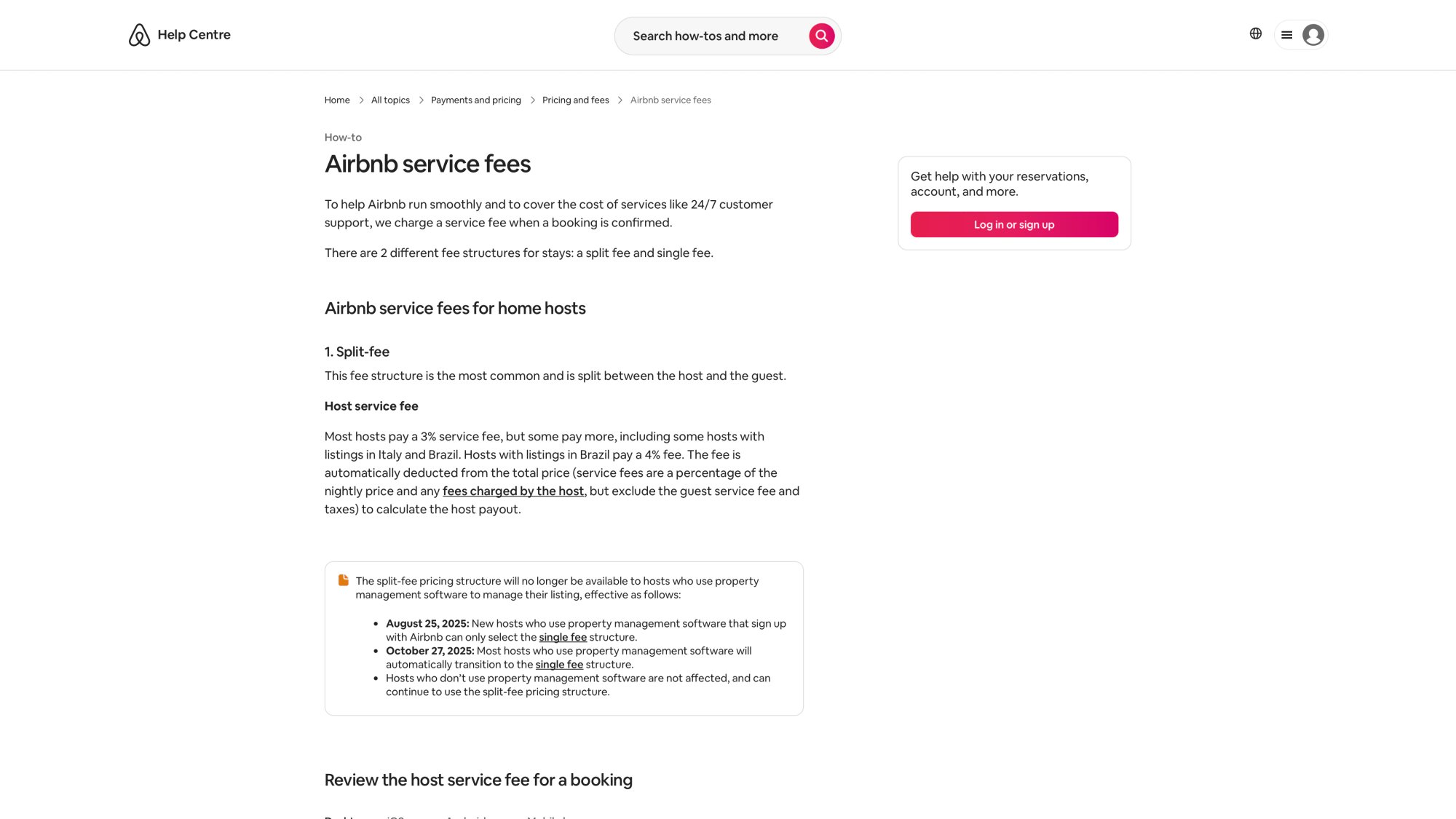

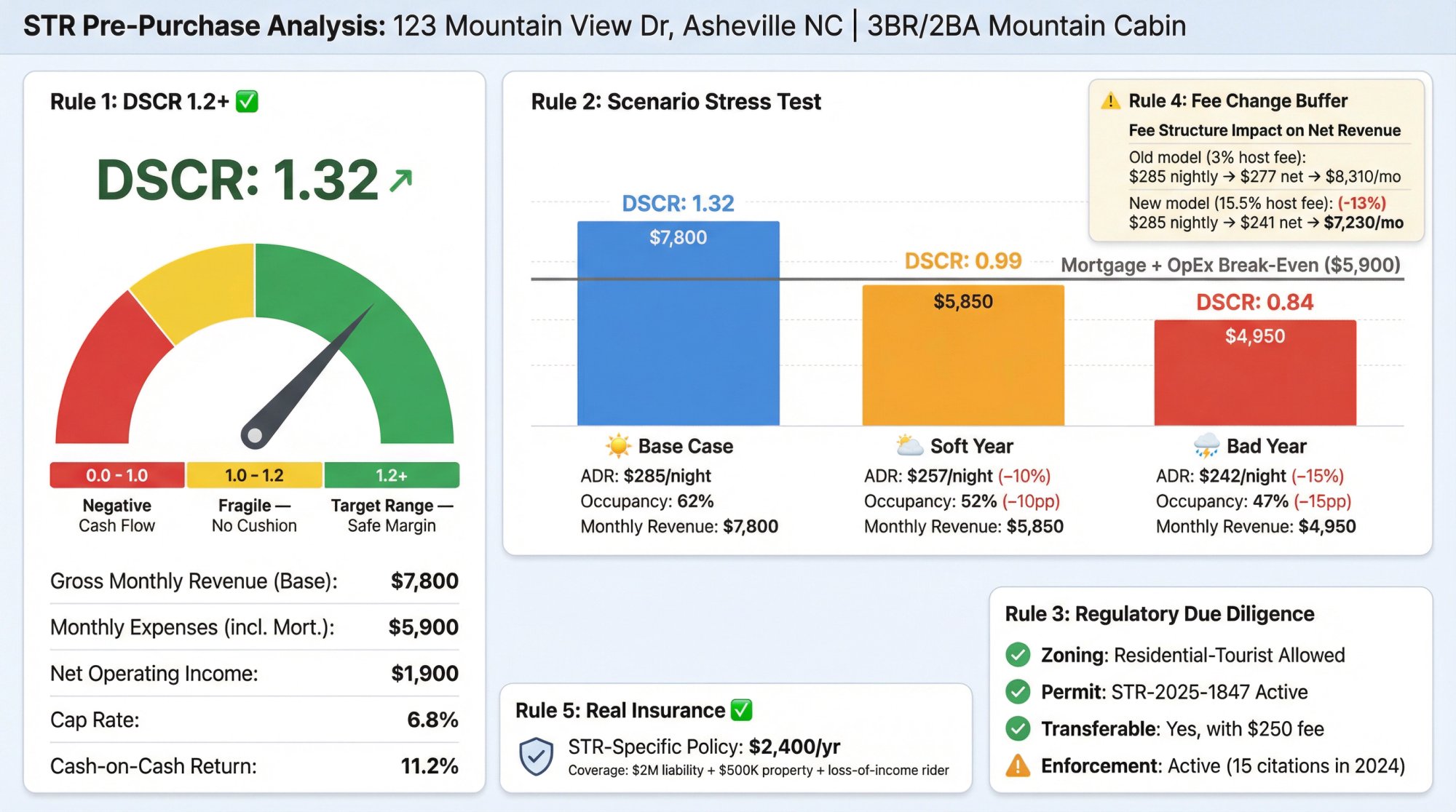

Understanding Airbnb's Split Fee vs Single Fee (3% vs 15.5%)

A lot of hosts are short because they're pricing against an outdated fee assumption. The math changed in ways many people didn't catch.

How Airbnb's Old Split Fee Structure Worked

Historically, the common setup was:

-

Host service fee around 3%

-

Guest service fee often 14.1% to 16.5% of booking subtotal (per Airbnb's help documentation)

Airbnb's New Single Host Fee at 15.5% (2025 Update)

Airbnb has moved many listings (especially software-connected hosts) to a single fee where the host pays the entire fee and the guest sees a cleaner price.

In August 2025, Airbnb announced that hosts using property management or channel management software would switch to a single fee of 15.5% deducted from the host's price.

Their example:

- If you keep your price at $100, you net $84.50 after the 15.5% fee.

Many operators are short by exactly the difference between "I thought my fee was 3%" and "I'm actually paying 15.5% now, and I didn't raise prices."

Important nuance: If you respond by raising prices mechanically, you might drop occupancy. The right move is to test price changes while tracking conversion and ranking, not blindly adding 15.5% to every rate.

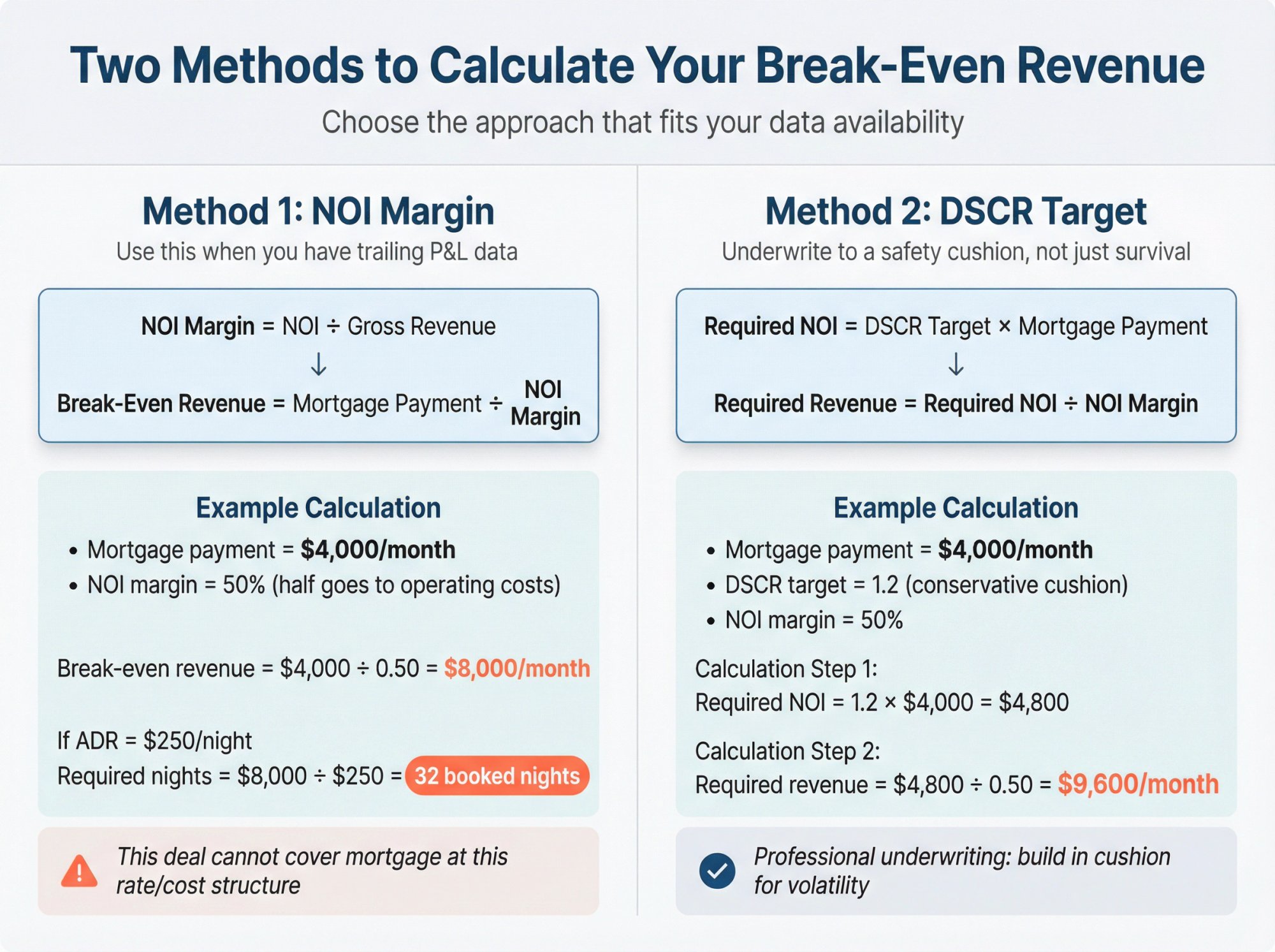

Calculate Your Break-Even Point: How Much Revenue You Need Monthly

You don't need more opinions. You need one number:

How much monthly revenue must this property generate to break even after real expenses?

There are two reliable ways to compute it.

Method 1: Calculate Break-Even Using NOI Margin

If you have a trailing P&L (or realistic estimate), calculate:

NOI margin = NOI / Gross Revenue

Then:

Break-even gross revenue = Mortgage payment / NOI margin

Example with illustrative numbers:

-

Mortgage payment = $4,000/month

-

NOI margin = 50% (half of revenue goes to operating costs)

-

Break-even revenue = $4,000 / 0.50 = $8,000/month

Convert to nights:

- If your ADR is $250, you need $8,000 / $250 = 32 booked nights

That's impossible in most months. This instantly tells you: this deal cannot cover the mortgage at this rate and cost structure.

Method 2: Calculate Break-Even Using DSCR Target

Set a target DSCR (conservative target: 1.2). Then solve:

Required NOI = DSCR target × Mortgage payment

Example:

-

Mortgage payment = $4,000

-

DSCR target = 1.2

-

Required NOI = $4,800

If your NOI margin is 50%:

Required revenue = $4,800 / 0.50 = $9,600/month

This is how professionals underwrite. You underwrite to a cushion, not to survival.

Chalet's market dashboards and calculator pair well for running these scenarios quickly with real market context.

7 Reasons Why Your Airbnb Isn't Covering Your Mortgage

1. You Based Projections on Peak Season Occupancy Rates

Markets are seasonal. Even "steady" cities have weekend/weekday cycles, event spikes, and off-season drops.

How to spot it:

Your best 2-3 months look fine. Your worst 2-3 months are brutal. The annual average looks okay, but your mortgage is monthly.

In reality, U.S. Airbnb occupancy averages around 50% in 2025, down from approximately 57% in 2024. Research shows this declining trend as new listings outpace demand.

The fix:

Underwrite to the worst quarter, not the best. Build cash reserves covering at least 3-6 months of the full payment. Chalet's market analytics can help you identify seasonal patterns in specific markets before you buy.

2. You're Comparing Against the Wrong Airbnb Properties

Two listings can have identical bedroom counts and totally different demand because of walkability, views, hot tub/pool, pet policy, parking, interior quality, group capacity, or permit status.

How to spot it:

You're priced "like comps," but your conversion is weak. Or you're cheaper than comps but still not booking.

The fix:

Rebuild comps around what guests actually buy. Chalet's analytics pages can help you see local performance patterns, but you still need comp logic at the property level.

3. Your Airbnb Operating Expenses Are Higher Than Expected

A property that grosses $7k can easily net $3k after real operating costs. Cleaning, utilities, and management fees add up faster than most people anticipate.

How to spot it:

Your gross looks okay. Your bank account doesn't.

The fix:

Treat expense control as a revenue strategy. If you save $300/month in utilities and supplies, that's equivalent to adding meaningful booked nights in many markets. Chalet's STR directory connects you with vetted property managers and cleaning services who can optimize your operations.

4. Airbnb Fee Changes Reduced Your Net Payout

Fees can change. Cancellation policies can change. Ranking can shift. The big one recently was the fee simplification and move to a 15.5% single host fee for many hosts. (Airbnb's resource center documents this transition.)

How to spot it:

Your bookings stayed similar, but your payouts dropped.

The fix:

Audit your payout math per reservation. Don't guess. Airbnb shows the host service fee in earnings for each booking. (Fee details are in their help documentation.)

5. Local STR Regulations Changed and Enforcement Increased

This is the risk most investors underprice.

New York City example:

NYC's Office of Special Enforcement reported that Local Law 18 and enforcement actions eliminated "tens of thousands" of illegal short-term rentals. Hosts must register, and platforms can't process transactions for unregistered listings.

Maui example:

Maui County signed Bill 9 into law in December 2025, aimed at phasing out transient vacation rentals in apartment-zoned districts over specific timelines.

You don't need to invest in those markets for this to matter. The lesson is universal:

Your ability to earn nightly revenue is partly a policy decision outside your control.

How to spot it:

Permits are unclear, neighbors complain, city council is active, enforcement is increasing, or your listing is "technically not allowed but everyone does it."

The fix:

Do a regulation check before you depend on the income. Chalet maintains a rental regulation library to speed up initial research (still verify with local authorities).

6. You're Treating AirCover as Mortgage Insurance (It's Not)

AirCover can help in specific cases, but it's not mortgage protection.

Airbnb's Help Center states that Host damage protection isn't an insurance policy, and not all damage is included. They suggest you also purchase personal insurance.

The Host Damage Protection Terms explicitly exclude or limit categories like wear and tear and list many ineligible losses.

How to spot it:

You're mentally counting on "Airbnb will cover it" for damage, downtime, or revenue loss.

The fix:

Treat AirCover as one layer, not the foundation. Real STR insurance decisions are part of staying solvent.

If you want to build a vetted ops and risk stack (insurance, PM, cleaning, tools), Chalet's STR partner directory is designed for that.

7. Your Mortgage Payment Is Too High for Realistic Airbnb Income

Sometimes it's straightforward: the debt load is too high for realistic NOI.

As of January 15, 2026, Freddie Mac's PMMS showed the average 30-year fixed-rate mortgage around 6.06%. (Compare that to rates around 3% in 2021 and approximately 7% in 2023, per Bankrate's historical data.)

Higher cost of debt raises the monthly payment. That shifts break-even occupancy upward.

How to spot it:

Even with excellent operations, you'd need unrealistic occupancy to cover the mortgage.

The fix:

This isn't an "optimize" problem. It's a structure problem. Down payment, purchase price, rate, term, or use case needs to change. Chalet's DSCR loan partners specialize in STR financing that focuses on property cash flow rather than personal income.

How to Fix Your Airbnb Mortgage Gap: 5 Proven Solutions

If your Airbnb isn't covering the mortgage, you have exactly five levers. Everything else is decoration.

Solution 1: Increase Airbnb Revenue Without Losing Bookings

High-impact moves that usually matter:

→ Reposition the listing (who it's for): families, remote workers, couples, groups, pet travelers

→ Upgrade what drives booking decisions: professional photos, sleep quality, fast WiFi, parking clarity, hot tub maintenance, noise policies

→ Minimum-night strategy: reduce turnovers in low season, raise average length of stay

→ Price strategy: test small changes, measure occupancy and booking window shifts

→ Distribution: diversify channels carefully (but remember AirCover only covers Airbnb stays)

Second-order effect to watch: Raising price to offset the 15.5% fee can lower occupancy, and your net can go down. You need to test, not assume. Use Chalet's calculator to model pricing scenarios.

Solution 2: Cut Airbnb Operating Costs Without Hurting Reviews

Cost-cutting that tends to work:

• Utility control: smart thermostats, leak sensors, water monitoring

• Cleaning efficiency: consistent team, clear checklist, linen systems

• PM renegotiation or hybrid management: pay for what you actually need

• Maintenance prevention: fix small issues before they become lost revenue weeks

If you need vetted help with cleaning, property management, maintenance, or tools, start with Chalet's STR tools and partner directory.

Solution 3: Switch to Mid-Term Rentals (30+ Days) for Stable Income

If your market has extreme seasonality or regulatory risk, one of the strongest stabilizers is mid-term rentals (30+ days) for traveling nurses, insurance displacement, or corporate stays.

This reduces turnovers and can stabilize occupancy. Chalet has a mid-term rental calculator for scenario testing.

Solution 4: Refinance Your Airbnb Mortgage or Change Loan Terms

This is where people jump too early. Do it after you know the real operating picture.

Paths you can explore:

① Refinance (rate/term)

② Extend amortization

③ DSCR refinance if you qualify

④ Remove PMI (if applicable)

⑤ Appeal taxes (jurisdiction-specific)

Many investors use DSCR loans because qualification is based more on property cash flow than personal income. Chalet connects investors with STR-aligned lenders and DSCR options.

Also note: conventional underwriting often treats rental income conservatively. Fannie Mae's selling guide describes how automated underwriting may use formulas like gross rent × 75% minus PITIA. Freddie Mac guidance indicates documented short-term rental income reported on Schedule E may be used for qualifying and must be annualized.

Translation: if you bought assuming a lender would "count projected Airbnb income," you might have been overconfident. Many lenders care about documentation and history.

Solution 5: Sell Your Underperforming Airbnb Before Losses Mount

This isn't defeat. It's capital preservation.

If the property can't reach DSCR 1.0-1.2 even after reasonable fixes, the correct move might be to:

• Sell

• Convert to long-term rental

• Reposition as personal use + partial rental

• Execute a 1031 strategy if applicable (talk to your qualified pros)

Chalet's "Airbnbs for sale" marketplace and agent network can help you understand what buyers will pay for cash-flowing versus underperforming properties.

How to Avoid Airbnb Mortgage Problems Before You Buy

If you want to avoid the "Airbnb not covering mortgage" outcome, use these rules.

Rule 1: Target DSCR of 1.2+ (Not Just Break-Even)

Break-even (DSCR 1.0) is fragile. A single bad month breaks you.

A conservative investor target is often DSCR 1.2+. Many lenders also commonly prefer DSCR in that range. (Research on DSCR refinancing from Chalet explains these thresholds.)

Rule 2: Run 3 Scenarios (Base, Soft Year, Bad Year)

Build a table like this:

| Scenario | ADR | Occupancy | Revenue Change | DSCR Result |

|---|---|---|---|---|

| Base | Your realistic assumption | Realistic | 0% | ? |

| Soft year | -10% ADR | -10 pp occ | Down | ? |

| Bad year | -15% ADR | -15 pp occ | Down | ? |

If you can't survive the soft year without personal cash injections, the deal isn't "cash flowing." It's "cash flowing when things go right."

Chalet's underwriting tool and calculator are useful for running these scenarios quickly.

Rule 3: Check STR Regulations Before You Buy

Don't just ask "is it allowed today?"

Ask:

• Is it allowed in this zoning?

• Is it permitted, licensed, and transferable?

• Is enforcement active?

• Is the city changing rules?

Use a regulation guide as a starting point, then verify with the local authority. (Chalet's regulation library can help speed up initial research.)

Rule 4: Assume Airbnb Fees Will Change (They Do)

Because fee structures can change (and have recently changed for many hosts), don't build a deal that only works if fees stay constant. (Airbnb's fee simplification announcement is a reminder of this risk.)

Rule 5: Get Real STR Insurance (Don't Rely Only on AirCover)

Airbnb itself says Host damage protection is not an insurance policy and doesn't cover everything. If your business depends on coverage assumptions, validate those assumptions with a real insurance professional.

Common Questions About Airbnb Not Covering Mortgage

Can Airbnb income cover a mortgage?

It can, but only if NOI supports the payment consistently. The mistake is thinking "gross bookings" equals "mortgage coverage."

You want NOI ≥ mortgage payment (DSCR ≥ 1.0), and ideally DSCR ≥ 1.2 for a cushion. (DSCR framework explained by Chalet.)

What if my payouts dropped suddenly?

Check whether your fee structure changed, especially if you use property management or channel software. Airbnb has moved many hosts toward a single fee and a 15.5% host service fee.

Does Airbnb cover lost income if something goes wrong?

AirCover has components like host damage protection and liability coverage, but it's not the same as business interruption insurance and has exclusions. Airbnb notes host damage protection is not an insurance policy and not all damage is included.

Can I use Airbnb income to qualify for a mortgage?

It depends on the loan and documentation.

-

Freddie Mac guidance indicates short-term rental income reported on Schedule E may be used and must be annualized.

-

Conventional underwriting often treats rental income conservatively and relies on documented history and formulas in the Fannie Mae selling guides.

-

DSCR loans often focus more on the property's cash flow, and many investors use them for STRs. Chalet connects investors with DSCR lenders.

What's the single biggest thing I should do next?

Run a real DSCR and break-even analysis with your true costs and realistic ADR/occupancy.

Chalet's Airbnb calculator is built for that workflow (free).

Are there markets where this problem is worse?

Yes. Cities like Phoenix and Austin saw significant increases in Airbnb listings over recent years, which contributed to substantial drops in revenue per listing from peak periods. Market research shows oversaturation effects in multiple markets.

About 31 of the top 50 STR markets saw occupancy declines recently due to oversupply. Chalet's market analytics help identify which markets are experiencing oversupply versus those with healthier supply-demand balance.

What about markets that still work?

Not every market is struggling. Some investors continue to see strong performance by focusing on:

• Year-round demand (business + leisure travel)

• Dual-season markets (ski in winter, lakes in summer)

• Markets with regulation clarity and supply caps

• Emerging secondary markets with 60-65% occupancy

The key is data-driven market selection, not following hot tips. Chalet's free analytics tools provide market-level insights to help identify promising locations.

What to Do Next If Your Airbnb Isn't Covering Your Mortgage

If You Already Own the Property

1. Run DSCR using trailing numbers, not hopes. (Use Chalet's free calculator.)

2. Identify whether the gap is revenue, expenses, debt structure, or regulation risk.

3. Choose one lever to pull first (revenue, expense, model change, debt change, or exit).

4. If you need operators (cleaning, PM, tools), use a vetted directory instead of random Googling. (Chalet's partner directory is designed for this.)

If You're Buying Your First Airbnb

1. Start with a market dashboard to understand demand patterns. (Chalet's analytics provide free market data.)

2. Run ROI and DSCR for the exact address. (Free calculator from Chalet.)

3. Check regulations before you fall in love. (Chalet's regulation library speeds up initial research.)

4. If you want a local pro who underwrites STRs correctly, connect with an Airbnb-friendly agent through Chalet.

If You're 1031 Exchanging or Building a Portfolio

You care about speed, certainty, and downside planning. Prioritize:

• DSCR cushion

• Regulation durability

• Operational redundancy (PM + cleaning bench)

• Financing options that match your entity structure

Chalet's lender matching for STR-focused programs can help you move faster.

The Bottom Line

The days when "any Airbnb covers the mortgage easily" have passed. Today's STR investors must combine realistic planning with active management.

If your Airbnb isn't covering the mortgage right now, use the situation as a learning opportunity and pivot point. Markets have shifted. Oversupply, higher costs, and fee changes created challenges for many hosts. But smart, data-driven hosts who stay flexible can absolutely thrive.

You have options. The worst move is doing nothing and hoping for the best. By understanding why things went off track, you can make savvy decisions to get back on course.