Short-term rental tax deductions are an incredibly powerful tool for hosts. They let you write off ordinary and necessary business expenses, which directly lowers your taxable income. This simple shift in thinking can turn tax season from a dreaded cost into a strategic opportunity to boost your annual profits.

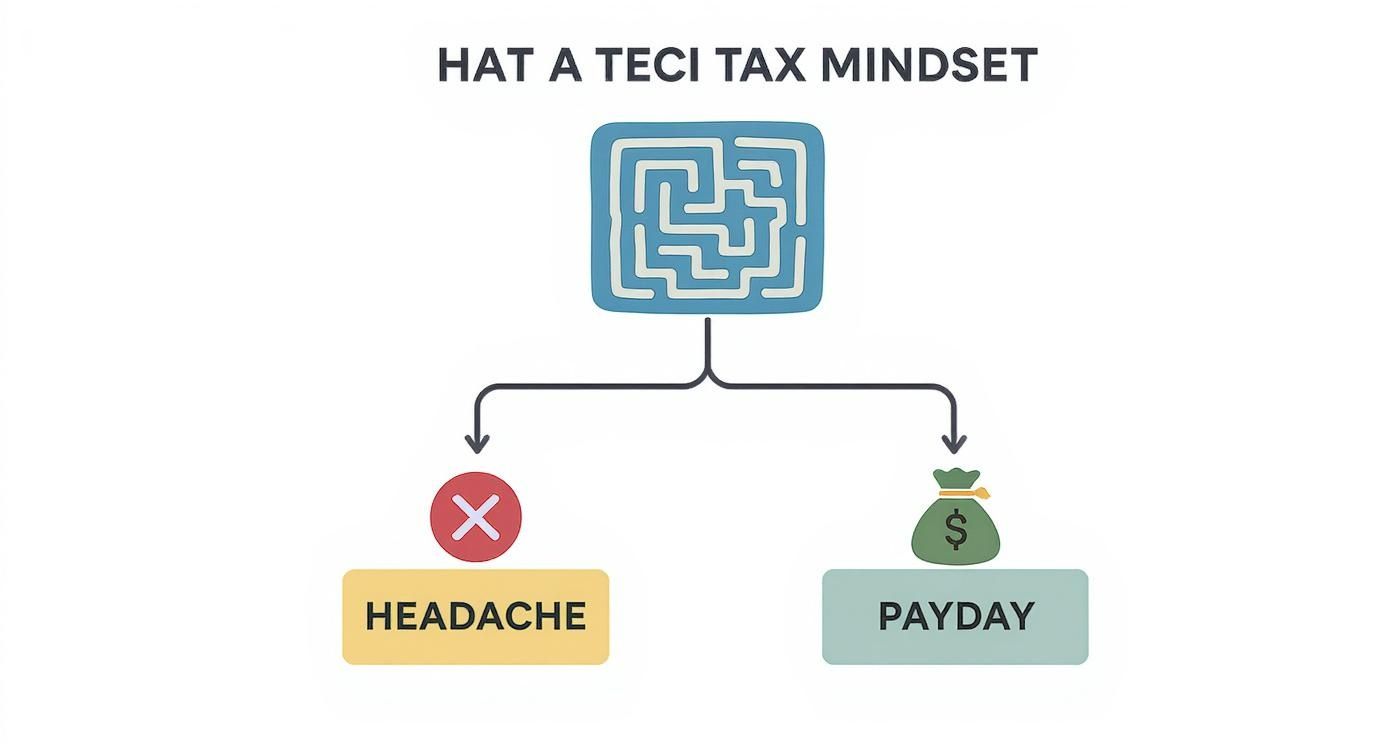

Turn Tax Season From a Headache Into a Payday

For a lot of short-term rental hosts, tax season feels like a tangled mess of confusing rules and missed chances. It’s all too easy to see it as an annual headache, a chore that just eats away at your hard-earned revenue. But what if you could flip that perspective on its head?

Smart tax planning isn’t just about staying compliant; it's one of the most effective strategies for increasing your bottom line. Every single legitimate deduction you claim is a dollar that goes straight back into your pocket instead of to the IRS. Start thinking of your rental not just as a piece of property, but as a small business with its own set of powerful financial advantages.

The key is shifting your mindset. Stop seeing taxes as a burden and start seeing them as a tool for building wealth. When you understand the short-term rental tax deductions available to you, you gain the power to actively shape your financial future.

Let's look at a quick, real-world story. Sarah, a new host, was ecstatic with her booking revenue after her first year. When tax time rolled around, she was ready to pay taxes on the full amount, completely unaware of the crucial write-offs she was entitled to. Luckily, after a quick chat with an advisor, she uncovered thousands in savings she had almost left on the table.

She was able to deduct expenses like:

- The portion of her mortgage interest and property taxes allocated to the rental.

- All the new furniture and smart TVs she bought to make her guests' stay more comfortable.

- Monthly subscriptions for streaming services and high-speed Wi-Fi.

- Even the professional photography she paid for to make her listing pop.

This guide is your roadmap to becoming like Sarah—confident, proactive, and financially savvy. We'll walk you through a clear, step-by-step path to understanding every potential write-off, from the small stuff like cleaning supplies to major property improvements. Our goal is to replace your tax anxiety with financial confidence, ensuring you never leave money on the table again. By the time you're done, you'll see tax season not as a chore, but as your annual payday.

Defining Your Rental for the IRS

Before you can touch a single deduction, you have to know how the IRS sees your property. Think of the tax code like a playbook with different rules for different types of players. How your rental is classified determines which playbook you use, and that directly impacts the short-term rental tax deductions you can claim.

How you use and operate your property slots you into one of three main categories, each with its own tax implications. Getting this right is the absolute first step to maximizing your savings. If you get this wrong, it’s like showing up to a football game with a basketball rulebook—you’re guaranteed to miss opportunities and probably get hit with a penalty.

This decision tree shows how your rental activity guides you toward either a tax headache or a strategic payday.

The bottom line is that your IRS classification is the critical first move. It’s what separates financial confusion from strategic gain.

Your Property's Tax Identity

The IRS doesn’t see all rentals the same way. The two big factors that determine your property’s classification are how many days you rent it out and the level of service you provide to guests. Let's break down the three main ways the IRS might see your property.

-

The "Tax-Free" Play (The 14-Day Rule): This is a unique sweet spot in U.S. tax law. If you rent out your property for 14 days or fewer during the entire year, you generally don't have to report that rental income. The catch? You also can't deduct any of your rental expenses. It’s a clean, simple trade-off.

-

Standard Rental (Schedule E): This is the most common classification. If you rent for more than 14 days and don't provide major, hotel-like services, the IRS sees your property as a standard rental. You'll report your income and expenses on Schedule E. This is considered a passive activity, which is a key term—it means your ability to deduct losses against other income (like your W-2 salary) is often limited.

-

Rental as a Business (Schedule C): If you're running your rental more like a hotel—providing substantial services like daily cleaning, meals, or concierge help—the IRS may classify it as a full-fledged business. This means you file on Schedule C, and your net income is subject to self-employment taxes. While that extra tax is a downside, the upside is huge: you can often deduct losses without the passive activity limitations that bog down Schedule E filers. For more on this, check out the insights from Rentastic.io on these classifications.

Your Ultimate Checklist of STR Tax Deductions

Alright, you've figured out your property's tax identity. Now for the fun part: finding every single dollar you can legally write off against your rental income.

The IRS keeps it simple in theory. You can deduct expenses that are both ordinary (common for your type of business) and necessary (helpful for running it). Think of this checklist as your roadmap to maximizing every single one of those short-term rental tax deductions.

We’ve broken this list down into common-sense categories to make sure you don't miss a thing. From the obvious big-ticket items to the small guest supplies, it all adds up to real tax savings.

Common Short-Term Rental Deductions at a Glance

Before we dive deep, here's a quick cheat sheet. This table breaks down the most common expenses you'll encounter as a host, giving you a bird's-eye view of what's on the table.

| Expense Category | Specific Examples | Key Consideration |

|---|---|---|

| Property & Operating Costs | Mortgage interest, property taxes, insurance, utilities, HOA fees. | These are your foundational, non-negotiable expenses. |

| Guest Experience | Cleaning fees, maintenance, toiletries, coffee, welcome gifts. | Anything that directly enhances the guest's stay is usually deductible. |

| Business Management | Platform fees (Airbnb/Vrbo), accounting software, legal fees. | The costs of running the business side of your rental are write-offs. |

| Repairs vs. Improvements | Fixing a leaky pipe (repair) vs. renovating a kitchen (improvement). | Repairs are deducted immediately; improvements are depreciated over time. |

This is just a starting point. Let's get into the nitty-gritty of each category to make sure you're claiming everything you're entitled to.

Property Essentials and Operating Costs

These are the core expenses tied to just owning and maintaining your rental property. They're usually the largest chunk of your deductions and are directly related to the physical building and keeping it running.

- Mortgage Interest: If you have a loan on your rental, the interest you pay is fully deductible. For most hosts, this is one of the biggest single write-offs of the year.

- Property Taxes: Those annual real estate taxes paid to your local government are a major deduction. Don't forget them.

- Homeowners Insurance: Your property and liability insurance premiums are a necessary cost of doing business, making them deductible.

- Utilities: The bills for electricity, gas, water, trash pickup, and internet are all deductible for the time the property is available for rent.

- HOA Fees: Is your property in a community with a homeowners' association? Those mandatory fees are a business expense you can write off.

Guest-Related Expenses

Crafting that perfect, five-star guest experience comes with costs. The good news? Those costs are almost always deductible. Anything you spend directly to make your guests' stay comfortable and memorable can help lower your taxable income.

For example, a host in the U.S. might deduct $5,000 in mortgage interest, $3,000 in property taxes, $1,200 in travel for property management, and $800 in maintenance in a single year. Each one of these directly chips away at your taxable income.

Here's a look at the most common guest-focused deductions:

- Cleaning and Maintenance: Fees paid to professional cleaners between stays are 100% deductible. This bucket also includes landscaping, pool service, and pest control.

- Supplies: Think about everything you stock for your guests: toilet paper, soap, shampoo, coffee, snacks, and even those thoughtful welcome baskets. The cost of these consumables is fully deductible.

- Repairs: Fixing a running toilet, patching a hole in the wall, or replacing a broken coffee maker are all deductible repairs that keep your property in top shape.

Key Takeaway: It's crucial to know the difference between a repair (deductible now) and an improvement (deducted over time). A repair brings something back to its original condition. An improvement enhances its value or extends its useful life.

Business Operations and Professional Services

Your short-term rental is a business, plain and simple. That means the costs of managing it—from marketing to accounting—are legitimate tax write-offs.

- Platform Fees: The service fees and commissions you pay to listing sites like Airbnb and Vrbo are fully deductible business expenses.

- Professional Services: Did you pay a lawyer to review your rental agreement? Or an accountant to handle your taxes? Those fees are deductible.

- Marketing and Advertising: The costs of promoting your property are write-offs. This includes professional photography, listing site fees, or even running social media ads.

- Office Expenses: You can also deduct costs like a dedicated business phone line, subscriptions to booking management software, or even a portion of your home office if you meet the requirements.

To make sure you're thinking like a true business owner and catching every possible write-off, you might find more ideas in this a complete guide to small business tax deductions.

Unlocking Your Biggest Tax Write-Off: Depreciation

While deducting operating costs is a great start, the single most powerful strategy in your tax toolkit is depreciation. It might sound like intimidating CPA-speak, but the idea is actually pretty simple.

Think about a new car. The second you drive it off the lot, it starts losing value. The IRS lets you deduct that loss in value—the "wear and tear"—on your rental property and everything inside it over time.

This isn't just about the building itself. You can depreciate nearly every major part of your rental, from the furniture and appliances to big-ticket items like the roof and HVAC system. The best part? It's a non-cash deduction. You don't have to spend a dime in a given year to claim it, yet it can slash your taxable income.

From a Slow Burn to a Massive First-Year Impact

Traditionally, you would write off a large purchase over several years. For example, the IRS might say new furniture has a five-year useful life. That means you'd deduct 20% of its cost each year. It’s a slow and steady way to get your tax savings.

But there's a much more potent tool that can supercharge your deductions: bonus depreciation. This special provision lets you accelerate those write-offs and claim them all in one year. Instead of a slow burn, you get an immediate, powerful impact on your tax bill.

Why 100% Bonus Depreciation is a Game-Changer

Imagine furnishing your entire rental—new beds, sofas, appliances, TVs—and deducting the entire cost on this year’s taxes. That's exactly what bonus depreciation lets you do.

This is a huge deal right now. The return of 100% bonus depreciation for short-term rental investments in 2025 creates a rare window of opportunity for hosts. This rule allows you to fully deduct the cost of qualifying property in the same year you put it into service. For instance, if you spend $15,000 on new furniture for your rental, you could claim the entire amount as a tax deduction in 2025. You can find more details about this powerful tax strategy on AirDNA.

This can create a massive "paper loss" in your first year, even if your rental is bringing in positive cash flow.

Example in Action:

Let's say you buy a property and spend $30,000 on furniture, appliances, and new flooring. With 100% bonus depreciation, you can deduct that entire $30,000 in year one. If your net rental income was $25,000, this deduction would wipe out your entire tax liability on the rental and create a $5,000 loss that could potentially offset other income.

Who Should Be Paying Attention to This?

Bonus depreciation is especially powerful for:

- New STR Owners: When you're first setting up a rental, the upfront costs are huge. This strategy allows you to immediately get a big chunk of that money back in the form of tax savings.

- Hosts Doing Major Upgrades: If you're tackling a big renovation—a new kitchen, updated bathrooms, or a full roof replacement—bonus depreciation can make that investment feel a lot more manageable.

By understanding and strategically using depreciation, you move beyond simple expense tracking and into the world of advanced tax planning. It’s one of the cornerstones of building real, long-term wealth with your short-term rental business.

Building an Audit-Proof Record-Keeping System

Even the most powerful short-term rental tax deductions are worthless without one critical thing: proof. If you can't back up your claims with clean records, you can't take the write-off. Simple as that.

Building an "audit-proof" system isn't about becoming a master accountant overnight. It's about creating a simple, organized way to track every dollar you spend on your rental business.

Think of it like building a case for your tax return. Every receipt, invoice, and bank statement is a piece of evidence. Your goal is to create an undeniable paper trail that makes your financial story clear, accurate, and instantly defensible if the taxman ever comes knocking.

This system doesn't need to be complex. A dedicated software is great, but even a basic spreadsheet works wonders. Consistency is what turns a shoebox full of receipts into a powerful tool for maximizing your savings and minimizing your stress. To really nail this, it helps to understand or use specialized property business accounts services.

What to Keep and How to Organize It

Your documentation is your defense. At a bare minimum, your system should track the date, vendor, amount, and business purpose for every single expense. This creates a clear picture of how you spent money to support your rental.

Here are the essential documents you have to keep:

- Receipts and Invoices: Hold onto everything, whether it's a digital copy or a paper one. This goes for big-ticket items like a new sofa all the way down to a bottle of cleaning spray.

- Bank and Credit Card Statements: These are crucial. They help you cross-reference your receipts and prove that payments were actually made.

- Mileage Logs: Driving for your rental business? You should be. Trips to check on the property, buy supplies, or meet a contractor are all deductible. Just keep a detailed log with the date, mileage, and purpose of each drive.

- Proof of Payment: This includes things like canceled checks, bank transaction records, or credit card slips that tie back to your expenses.

The easiest way to organize this is digitally. Create folders labeled "Utilities," "Cleaning," "Repairs," and "Marketing" and sort your records by category and date. Come tax time, you'll thank yourself.

The golden rule from the IRS is to keep records for at least three years from the date you file your return. A clean, digital backup system makes this completely painless.

Splitting Expenses Between Personal and Rental Use

This is where so many hosts get tripped up. If you use your property for personal getaways—even for a weekend—you can't deduct 100% of your annual expenses. The IRS requires you to allocate costs based on how many days the property was used for personal stays versus rental stays.

Here’s the straightforward, IRS-approved method for getting it right:

- Count Your Total Usage Days: Add the number of days you personally used the property to the number of days it was rented out at a fair market price.

- Calculate the Rental Use Percentage: Divide the number of rental days by the total usage days from step one.

- Apply the Percentage: Multiply your total eligible expenses (like mortgage interest, property taxes, and utilities) by this percentage. The result is your final deductible amount.

Let’s say you rented your property for 200 days and used it personally for 50 days. Your total usage is 250 days. Your rental use percentage is 80% (200 ÷ 250). That means you can deduct 80% of your shared expenses for the year.

Common Questions About STR Tax Deductions

Even with a clear roadmap, the world of short-term rental tax deductions can have some tricky intersections. Let's tackle the most common questions and nuanced scenarios hosts run into.

Think of this as a final consultation to clear up any lingering doubts before you file.

Can I Deduct Expenses for a Property I Also Use Personally?

Yes, but you have to be incredibly meticulous about how you allocate the costs. The IRS is very clear on this: you must divide expenses based on the number of days the property was used for personal enjoyment versus the number of days it was rented out at a fair market rate.

Let's break it down with an example. Say you used your beach house for 30 personal days and rented it for 120 days. That's 150 total usage days. This means you can generally deduct 80% (120 ÷ 150) of your shared expenses like mortgage interest, property taxes, and utilities.

Keeping a detailed log of personal versus rental days isn't just a good idea—it's absolutely essential for this calculation to hold up.

Are Fees from Platforms Like Airbnb and Vrbo Deductible?

Absolutely. Every single dollar you pay in service fees, host commissions, and other charges to listing platforms like Airbnb or Vrbo is 100% deductible. These are considered ordinary and necessary business expenses.

Thankfully, these platforms make it pretty easy. They typically provide annual income summaries that clearly itemize your gross earnings and the fees they've charged. This documentation makes it straightforward to claim these deductions on your return.

Important Reminder: Never overlook these fees. While they may seem small on each individual booking, they add up to a significant—and fully legitimate—write-off over the course of a year.

What Happens If My Rental Expenses Exceed My Income?

When your expenses are greater than your income, you have a rental loss. But whether you can deduct that loss against other income (like your salary) gets complicated fast, thanks to what the IRS calls "passive activity loss" rules. For most people, the ability to write off these losses is limited.

However, there are two primary ways around this limitation:

- Active Participation: If your modified adjusted gross income falls below a certain threshold, you might be able to deduct up to $25,000 in losses. The key here is that you must be actively participating in the rental's management.

- Real Estate Professional Status: This is the holy grail for some investors, as it allows for unlimited loss deductions. But be warned: the requirements are very strict and time-intensive, and it's not a status you can claim lightly.

Given how complex these rules are, if you find yourself with a significant rental loss, your best move is to talk to a tax professional. They can help determine your eligibility and make sure you navigate the rules correctly to get every deduction you're entitled to.

Navigating the complexities of STR investments, from market analysis to tax strategy, requires the right data and a team of experts. Chalet provides the free tools and professional network you need to analyze, buy, and manage your properties with confidence. Explore our free analytics and connect with STR-specialist agents today at https://www.getchalet.com.