The real estate and Short-Term Rental (STR) markets are experiencing a series of fluctuations, with investor home purchases and new home sales witnessing a decline.

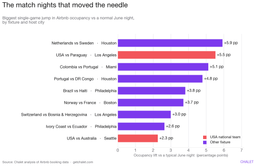

However, amidst these shifts, July 2023 marked a record-breaking month for the STR market, with 35.4 million nights stayed in the U.S., showcasing the market’s resilience and potential for growth.

1. Investor Retreat and Market Dynamics:

Investor home purchases have seen a 45% decrease YoY in Q2 2023, with investor market share falling to 16% from a peak of 20% in early 2022. This retreat is most significant in booming Sun Belt metros like Phoenix and Las Vegas. Despite this, some metros like Miami, San Francisco, and San Jose are showing promising trends, with Miami having the highest investor market share at 30%.

A Closer Look at Metro Dynamics:

In cities like Phoenix and Las Vegas, the decline in investor activity is particularly pronounced, signaling a shift from the boom experienced during the pandemic.

However, contrasting trends are emerging in cities like Miami, where investor market share remains robust. Understanding these metro-level dynamics is crucial for investors seeking to identify opportunities and adapt strategies.

2. Mortgage Rates Impact and Home Sales:

Rising mortgage rates, reaching above 7%, have impacted the housing market, pushing many potential buyers out of the market and contributing to a decline in new home prices. The lack of inventory has particularly impacted existing home sales, which slid 0.7% in August from the previous month to an annual rate of 4.04 million units, a 15.3% decrease compared with August 2022.

The Ripple Effect of Mortgage Rates:

The surge in mortgage rates has created a ripple effect across the market. Sellers who secured low mortgage rates before the pandemic are now reluctant to sell, contributing to inventory shortages. This scenario underscores the interconnectedness of market factors and the importance of staying informed about broader market trends.

Top 500 Airbnb Rental Markets

Instantly compare the top 500 short-term (Airbnb) rental markets in the US

3. STR Market Resilience:

Despite the challenges, the STR market demonstrated resilience with July 2023 breaking the record for the most STR stays in one month in the U.S.

The searing heatwave and increased interest in off-season booking are expected to keep demand high in the coming months, presenting opportunities for investors focusing on the rental market.

Seasonal Trends and Market Adaptation:

The STR market is showcasing adaptability with increased interest in off-season booking, indicating a diversification of demand. Investors can leverage this trend by aligning their offerings with seasonal preferences and exploring untapped markets, thereby maximizing revenue opportunities.

4. Diverse Investor Strategies:

Investors are adapting to the changing landscape by focusing on low-priced homes, single-family homes, and rental properties. The strength of the rental market and high asking rents provide opportunities for investors who are landlords, especially in cities witnessing high investor market shares and median sale prices.

Strategic Adaptation and Market Positioning:

In a dynamic market, strategic adaptation is key. Investors are exploring various property types and focusing on the rental sector to navigate market shifts. By staying agile and aligning strategies with market trends, investors can position themselves for success and capitalize on emerging opportunities.

5. Conclusion:

The real estate and STR markets are dynamic, with shifts in investor activity, mortgage rates, and market trends. By staying informed, adapting strategies, and leveraging market resilience, investors can navigate the tides, uncover opportunities, and position themselves for success in this evolving landscape.

Final Thoughts

In a market characterized by change, knowledge is power. Investors equipped with insights into market dynamics, investor behavior, and emerging trends are better positioned to make informed decisions and seize opportunities.

The record-breaking STR stays in July 2023 and the diverse trends across metros underscore the potential that lies within the market, waiting to be uncovered by savvy investors.